Most privately-held businesses created and registered before January 1, 2024 are required to file beneficial ownership information (BOI) with the Financial Crimes Enforcement Network (FinCEN), which is a part of the U.S, Department of the Treasury (DOT), by January 1, 2025.

For businesses created or registered after January 1, 2024, but before January 1, 2025, filing is required within 90 days after receiving actual or public notice that the creation or registration has become effective.

Reporting businesses created or registered after January 1, 2025 must file within 30 days of actual or public notice that the creation or registration has become effective.

For all reporting businesses created or registered after January 1, 2024, the BOI reporting requirements extends to “company applicants” as well (see below for specifics concerning “company applicants”). This requirement does not apply to businesses created and registered prior to January 1, 2024.

Several members of the U.S. House of Representatives have pleaded for a delay to the effective date of this reporting requirement, but to no avail.

While litigation against implementation of this reporting requirement is ongoing (see below), we recommend you be prepared to file these reports ahead of the deadline, as there is no guarantee that the courts will resolve every lawsuit before the deadline, nor that a nationwide preliminary injunction will be issued.

Does This Reporting Requirement Apply to Your Business?

If your business is a U.S. entity:

If your business is a U.S. entity:

- Created under U.S. laws (which include state and Native American tribal laws);

- A corporation or LLC; and

- Created via filing of a document or documents with a secretary of state or similar office or

Your business is an entity:

- Created under the laws or a foreign nation; and

- Registered to do business in any U.S. State or Tribal jurisdiction via filing of a document or documents with the secretary of a U.S. State or similar office

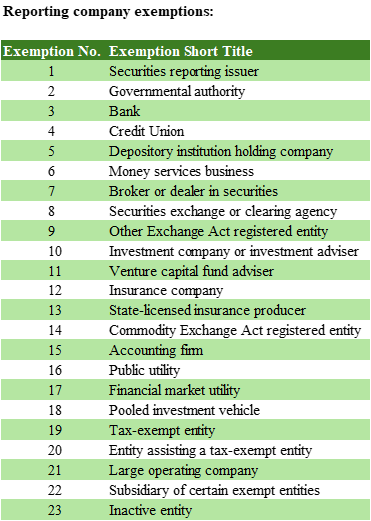

Unless you work in one of the exempted industries – click here for the full exemption list – you may have to file BOI reports with FinCEN.

What Constitutes Beneficial Ownership?

“Beneficial owners” are those individuals who, directly or indirectly, either:

“Beneficial owners” are those individuals who, directly or indirectly, either:

- Exercise substantial control over your business, or

- Own or control at least 25% of the ownership interests of your business.

Sounds simple? Well, it’s not. There are many criteria by which FinCEN may deem a person to exercise “substantial control” over a business. These include:

- Senior officers (e.g., president, chief financial officer, general counsel, chief executive officer, chief operating officer).

- Anyone who can appoint or remove a senior officer or a majority of the board of directors.

- Important decision makers, who include those with direction or determination of, or substantial influence over, the business, its finances, or its structure.

Determining whether an individual qualifies as a beneficial owner can be complicated. A further potential complication is that “beneficial ownership” covers those who exercise any other form of “substantial control” over the business in addition to the above categories. This is very vague wording; we hope future guidance will provide more specific criteria to identify what those other forms of substantial control represent in practice.

Further, the “beneficial ownership” status includes those individuals who control an intermediary entity that exercises “substantial control” over the reporting business.

There are exceptions, such as for minor children who may, through inheritance or gift, possess sufficient ownership of the reporting business to qualify. In this case, the requirements would allow for reporting such information about the parent or legal guardian of the child in question.

For businesses created or registered after January 1, 2024, which must follow the reporting requirements for “company applicants,” company applicants are those individuals who directly file the documents creating domestic or registering foreign reporting businesses, as well as those who exercise primary responsibility for directing or controlling the filing of the creation or first registration documents.

Again, for businesses created or registered before January 1, 2024, FinCEN does not require the filing of BOI for company applicants.

What Beneficial Ownership Information Does FinCEN Require?

If your business is a “reporting business,” as defined by the rule, FinCEN requires you to report:

If your business is a “reporting business,” as defined by the rule, FinCEN requires you to report:

For the reporting business itself:

- Full legal name.

- Any trade name or “doing-business-as” (“DBA”) name.

- Complete current U.S. address of the principal place of business.

- Jurisdiction (state, tribal, or foreign) of formation; and

- IRS taxpayer identification number (TIN).

For foreign reporting businesses, the required information includes the state or tribal jurisdiction of the first U.S. registration to do business in this country. If a foreign company does not have an IRS issued TIN, FinCEN requires a foreign-issued TIN and the name of the issuing jurisdiction.

For each individual with “beneficial ownership interest,” including “company applicants” for those reporting businesses created or registered after January 1, 2024, FinCEN requires:

- Full legal name.

- Date of birth.

- Complete current address.

- Unique identifying number (e.g., Social Security number); and

- An image of a U.S. passport, a state driver’s license, or a state identification document or card. A foreign passport is accepted for those who may have none of these.

This represents only an overview of the new FinCEN reporting requirements, not a complete explanation of every aspect.

Litigation: Current Status

On March 1, 2024, in National Small Business United d/b/a the National Business Association, et al. v. Janet Yellen, in her official capacity as Secretary of the Treasury, et al., U.S. District Court Judge Liles Burke (Northern District of Alabama) granted summary judgment banning enforcement of the FinCEN reporting requirements, ruling that the CTA is unconstitutional – but only as applied to the named Plaintiffs in the case.

On March 1, 2024, in National Small Business United d/b/a the National Business Association, et al. v. Janet Yellen, in her official capacity as Secretary of the Treasury, et al., U.S. District Court Judge Liles Burke (Northern District of Alabama) granted summary judgment banning enforcement of the FinCEN reporting requirements, ruling that the CTA is unconstitutional – but only as applied to the named Plaintiffs in the case.

These consist solely of the National Small Business Association and its members (some 60,000-plus, representing ~0.1%-0.2% of the small business owners FinCEN reporting requirements would have applied to), plus Isaac Winkles and any reporting companies in which he has beneficial ownership interests.

On behalf of the DOT, on March 11, 2024, the Department of Justice filed a Notice of Appeal, sending the case to the U.S. Court of Appeals for the Eleventh Circuit, which agreed to hear the appeal. The Court heard oral arguments on September 27, 2024, and is proceeding on an expedited timeline, but, as we noted above, there is no guarantee that a decision will be reached in any specific timeframe.

Further, whatever the decision may be, or whenever it may be reached, that almost certainly won’t be the final word – the losing side, whether it is the DOT or the National Business Association, et. al., is very likely to appeal the verdict to the Supreme Court and, absent the issuance of a nationwide injunction, preliminary or otherwise, the reporting requirements will likely remain in effect for most businesses.

Other lawsuits against the DOT implementing this reporting requirement include:

- Black Economic Council of Massachusetts, Inc. (BECMA) et. al. v. Yellen et. al. (filed 5/29/2024)

- National Federation of Independent Businesses (NFIB) et. al. v Yellen et. al. (filed in Texas 5/28/2024)

- William Boyle v. Yellen et. al. (filed in Maine 3/15/2024)

- Small Business Association of Michigan et. al. v. Yellen et. al. (filed 3/1/2024)

- Robert J. Gargasz Co., L.P.A. et. al v. Yellen et. al. (filed in Ohio 12/29/2023)

Again, we would strongly encourage you to confer with your CPA or Virtual CFO as well as your business attorney to ensure your business is ready to comply with the new reporting requirements in advance of the reporting deadline.

If you have any questions about the FinCEN reporting requirements, please click here to email us directly – let us help you, that’s what we’re here for!

Until next time –

Peace,

Eric

{kind=link}